Although there are exceptions, in general, owning becomes cheaper than renting if you are going to live in the area for more than 2-3 years. That’s when the cost savings keep increasing relative to renting, in addition to appreciation which you don’t get when renting.

The math of buying vs. renting in the Greater Boston area:

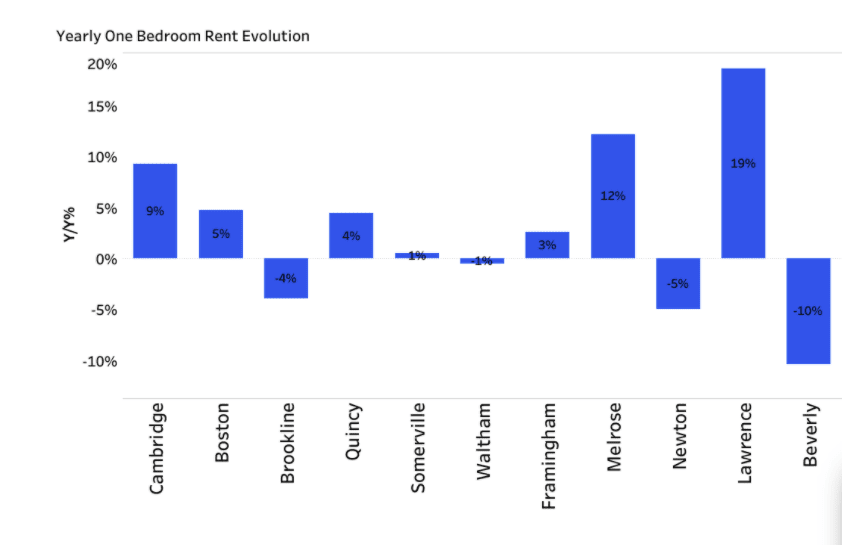

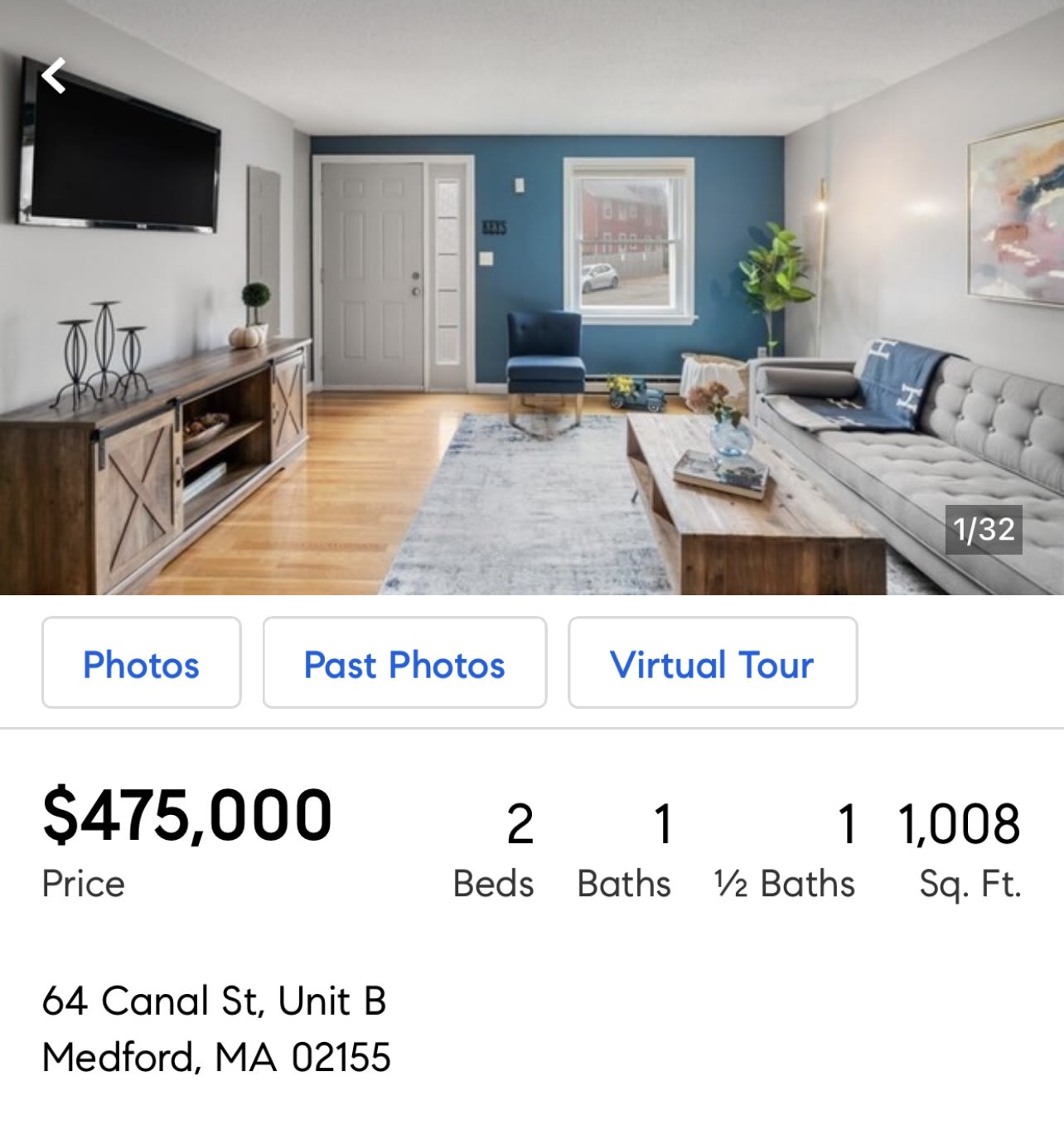

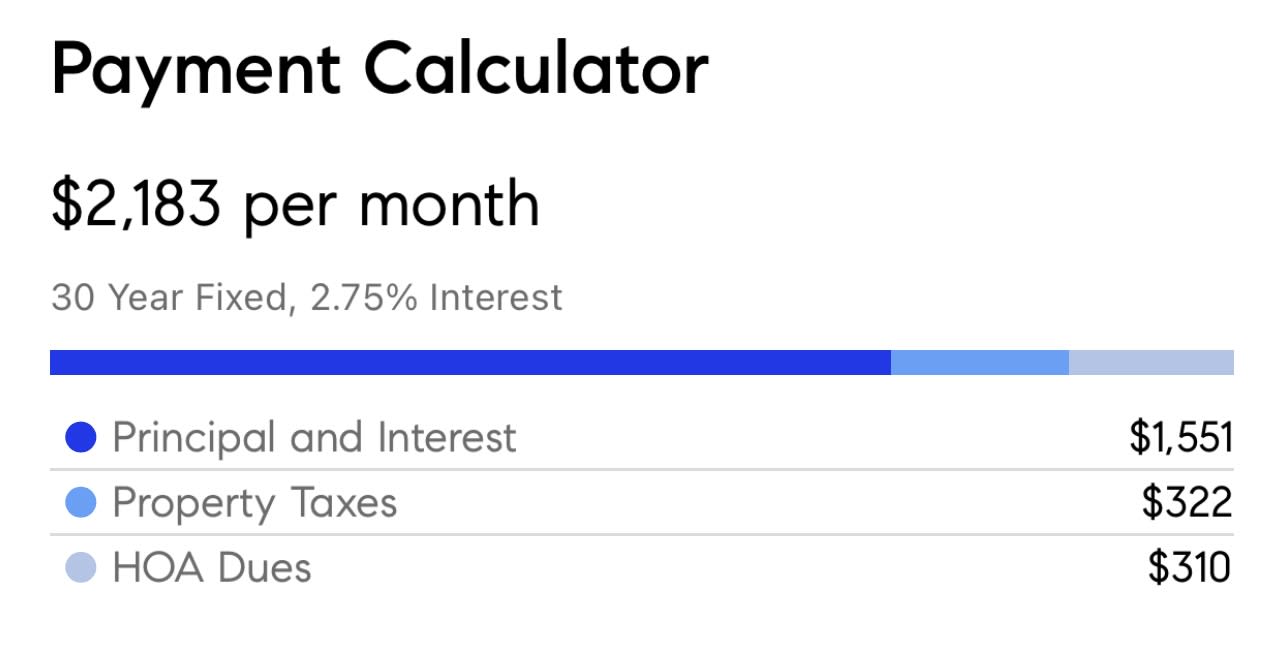

Take this $475,000 two-bed condo in Medford as an example. Monthly payment at 20% down payment with 2.75% interest is $2,183 including HOA fees and property taxes. That's about the same the the median 2 bed rent in Medford in the past 6 months which was $2250 (source: MLS, this article was last updated on 10/27/2021). The monthly payment of home ownership goes towards building equity and the home owner also benefits from appreciation. And when the interest rates go down, the home owner can refinance to lower the monthly payment. In contrast, the Boston rents have historically gone up over time. According to a Zumper article published this October, Cambridge 1 bed rent increased by 9%, while Boston has increased by 5% in the past year. Demand in the city has gone back up as more people get tired of the commute and move back.

In addition, the Medford housing market appreciated 12.1% in the past 12 months (source: Zillow Home Price Index). That's $57,475 appreciation of a $475,000 in one year that a renter misses.

There are several tax benefits of home ownership.

Mortgage Interest and Local Tax Deduction: Interest paid on the first $750,000 of the loan amount on your primary residence or second home is tax-deductible, as are the real estate taxes, up to certain limits.

Owner-occupied exclusion: If you sell a home you lived in for two out of the past five years, you can claim an exemption from capital gains tax. This tax exemption applies to the first $250,000 of price gain if you are single, and $500,000 if you are married. If you have lived in your home for long enough for the value to double, you may want to consider selling your home and buying a different one of the same value so you won't have to pay tax on the next $250,000 or $500,000 of appreciation.